Typically, checking accounts also come with a debit card for easy access to funds. Accounts receivable (AR) is the money your customers owe you for products or services they bought but have not yet paid for. It’s important to track your AR to ensure you receive payment from your customers on time. Generally, if your assets are greater than your liabilities, your business is financially stable. Note that certain companies, such as those in service-based industries, may not have a lot of equity or may have negative equity.

- Some of these elements are done more regularly than others to ensure that the books are always up to date.

- Recording a financial transaction in your general ledger is referred to as making a journal entry.

- When manually doing the bookkeeping, debits are found on the left side of the ledger, and credits are found on the right side.

- Centuries ago, businesses would record their financial transactions in a physical book called the general ledger (GL).

- With this credit, you can get up to $26,000 back per employee during COVID-19.

Why Do Small Businesses Need Bookkeeping?

This happens when you transfer money from one of your business accounts to another one or to a business credit card. After all, if you don’t know how much you’re making or where that money is going, you’ll have a hard how to adjust journal entry for unpaid salaries time finding ways to expand your profitability. Consider using one of the best bookkeeping services to make managing your books a breeze.

Choose an Accounting Method

Most accounting software offers a range of features that are suited for almost any type of small business. If your business chooses to keep this task in-house, it’s best to stick to a predictable expense tracking schedule. Developing a bookkeeping routine prevents you from accidentally forgetting important steps in the accounting process. Bookkeeping software helps you prepare these financial reports, many in real-time. This can be a lifeline for small-business owners who need to make quick financial decisions based on the immediate health of their business.

The best bookkeeping software syncs with your business bank account and payroll systems so that you’re easily able to import and export transaction history. We’ll cover some of the best business bookkeeping software options a little later. Since good record keeping relies on accurate expense tracking, it’s important to monitor all transactions, keep receipts, and watch business credit card activity. Many bookkeeping software options automate the tracking process to eliminate errors. When you keep detailed, organized records of your business transactions, tax season suddenly won’t feel like such a daunting chore. By being proactive with your bookkeeping, you’ll save your small business time when it comes to taxes.

The 3 golden rules of bookkeeping to follow

More commonly, entrepreneurs use comprehensive accounting software like QuickBooks that can handle a larger volume of transactions and provide a deeper analysis. QuickBooks Live Expert Assisted can help you streamline your workflow, generate reports, and answer questions related to your business along the way. Bookkeeping is simply the bookkeeping terms process of recording all the money that goes in and out of a business. It used to involve entering information into ledger books – hence the name – but most businesses now do it using accounting software. Manually recording transactions by hand is the most time-consuming option for recording transactions.

Keep a separate bank account for your personal and your business expenses. If you’re a solopreneur or independent contractor, chances are you’re responsible for everything, including the accounting. To avoid confusion during tax season, set up a separate schedule b form report of tax liability for semiweekly schedule depositors bank account for your business.

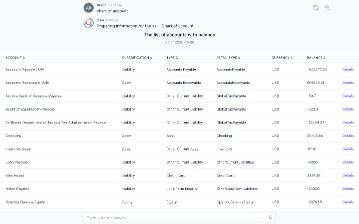

The most common small-business accounts

This chart of accounts is used to gather statements, analyze progress, and locate transactions. Once your business is registered and starts making transactions regularly, it’s time to prepare the bookkeeping system for your business. The financial books allow you to review your income and expenses, take control of your finances and make smart decisions.

Single-entry bookkeeping is simpler, and is usually used by businesses with few or no employees, minimal plans to scale, and no need for in-depth financial reporting. If you choose to use double-entry bookkeeping—and we strongly suggest you do! We’ll show you examples of how to record a transaction as both a credit and debit later on. Based on the monthly sales, set aside some money to pay for your taxes.

Or you may choose a more traditional approach and have your fiscal year follow the standard calendar year, depending on what works best for your business. If you operate a seasonal business, for instance, then you may choose to begin your fiscal year at the beginning or end of your peak sales season. Andy Smith is a Certified Financial Planner (CFP®), licensed realtor and educator with over 35 years of diverse financial management experience.

No Response to "Accounting for Small Businesses: A Comprehensive Guide to Financial Management"