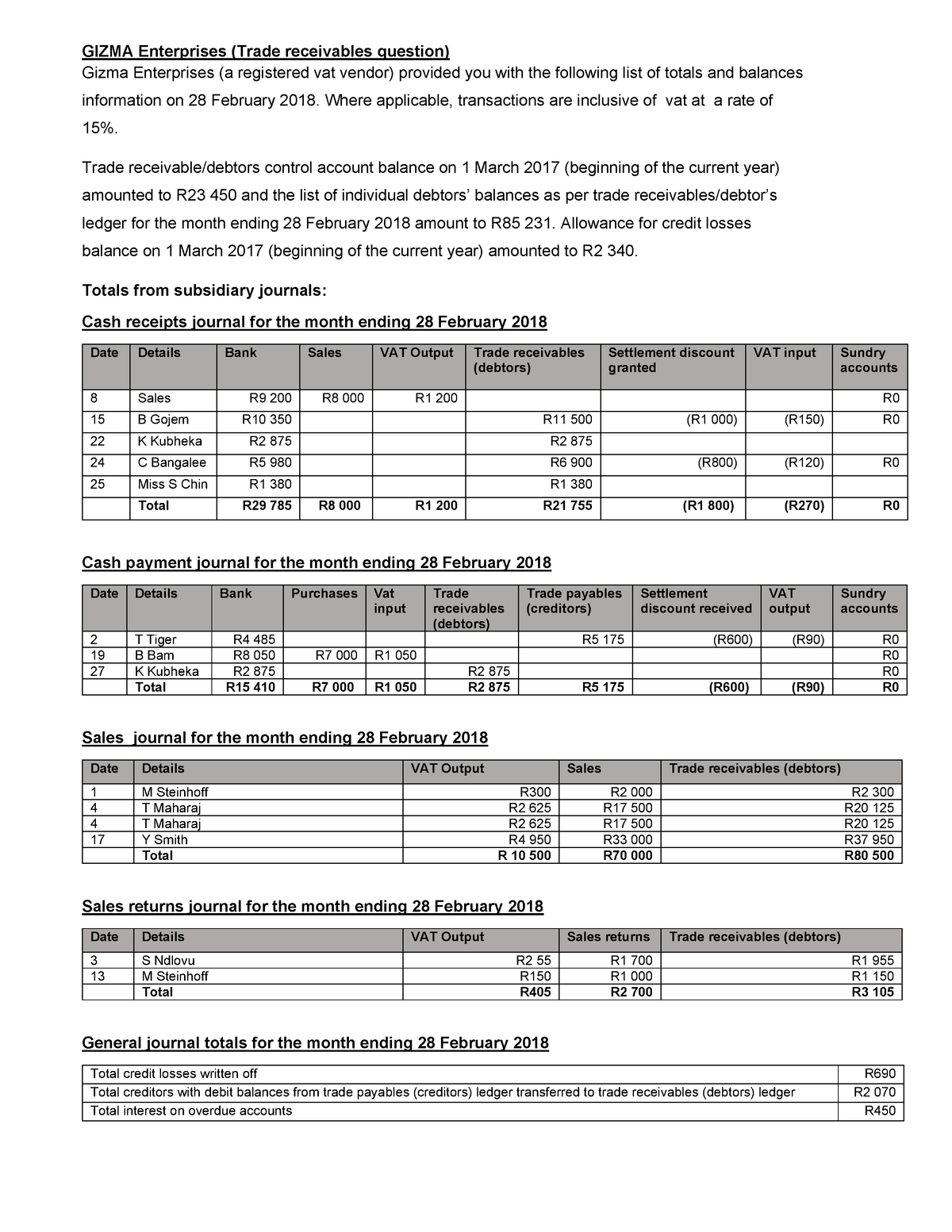

Past week’s Government Set aside price reduce features led to a new opportunity for homeowners to secure alot more favorable home loan rates . Throughout the weeks before brand new slashed, financial costs started initially to shed, having lenders preemptively costs on the asked protection. This resulted in mortgage pricing shedding to help you a two-season low off six.15% , easing a number of the economic pressure to the homebuyers.

While you are good six.15% mortgage speed may not be as tempting as step three% prices which were considering when you look at the pandemic, it still represents a critical improvement on latter element of 2023, when financial costs was basically hovering dangerously nearby the 8% draw . Nevertheless the fifty-basis-part speed slashed established from the Fed, and this exceeded many analysts’ traditional by twofold, next expidited the new downward development, best mortgage pricing to fall to normally 6.13% , in which it already sit.

For potential homebuyers, which shift in the market gift ideas an opportune second so you can secure when you look at the a great price towards an interest rate. Yet not, while you are aiming to safer a far more advantageous rates, there are some procedures you are able to so you can possibly protected a mortgage rate out-of 6% otherwise straight down today.

Purchase mortgage issues

Perhaps one of the most easy a method to decrease your financial speed is through to invest in home loan affairs . A mortgage part is basically an upfront commission you have to pay in order to the bank in the closing to minimize your interest rate over the longevity of the mortgage. One-point typically will set you back step one% of loan amount and generally minimises your interest rate by the 0.25%, even when this payday loans Eunola no credit check can will vary by the financial.

Instance, if you are searching in the good $300,000 home loan having a great six.13% interest rate, buying one point manage charge a fee $step three,000 but could bring your speed down seriously to around 5.88%. The greater facts you buy, the greater you lower your speed – even in the event, needless to say, so it includes a top upfront rates.

However, it is essential to assess how much time you intend to stay in your residence with regards to this 1. If you plan in which to stay the house for several years or higher, the brand new initial costs will be well worth the savings you’ll collect away from a lower life expectancy payment. In case you aren’t thinking about way of living indeed there with the long identity, the expense of buying circumstances will get exceed the eye savings.

Choose a beneficial fifteen-year home loan

A unique approach to protecting a reduced financial rate will be to like an excellent 15-12 months mortgage instead of the antique 30-season mortgage. At this time, rates with the fifteen-seasons mortgage loans was averaging as much as 5.49%, that’s rather less than new 6.13% average to own 29-12 months mortgage loans.

A smaller-label financing means you are paying the borrowed funds reduced , hence typically translates to less chance to your bank. Therefore, lenders reward consumers with straight down interest rates. The newest disadvantage is that the monthly payment could be high because you may be paying the mortgage in two the amount of time, however the complete offers during the attract over the lifetime of the mortgage can be big.

Such as, to your an effective $300,000 home loan, good fifteen-seasons loan from the 5.49% would have large monthly obligations than simply a 30-seasons loan from the six.13%, but you would shell out not as into the interest complete and construct guarantee faster . If you have the financial flexibility to cope with a higher month-to-month payment, this will be perhaps one of the most effective ways to score a beneficial mortgage rate lower than six%.

Think an arm financing

Adjustable-rate mortgage loans (ARMs) offer another way to safer a lowered rate. As opposed to fixed-speed mortgages, Palms give an introductory period in which the rate of interest is fixed, basically for 5, eight otherwise a decade. Up coming, the loan rates changes a-year centered on market conditions.

An important benefit of a supply is the down very first speed, hence averages 5.77% currently. And you will since of many experts expect then Fed price slices in the the future, it will be possible that mortgage costs you will get rid of further , and make Arms an appealing choice for those individuals willing to take on a bit more exposure.

However, it’s important to be cautious which have Sleeve funds , since price also increase pursuing the repaired months stops (with respect to the overall rates environment). This means your instalments you will go up rather when the interest rates go afterwards. But in a slipping speed ecosystem, for instance the that the audience is currently during the, a supply could possibly offer large coupons for the ideal borrower.

The conclusion

When you are the current financial cost are much even more advantageous than they certainly were just a few days in the past, smart customers may be able to force their costs actually straight down by utilizing the brand new methods in depth over. Each of these tactics boasts a unique advantages and disadvantages, so it’s vital that you examine the enough time-name economic wants, chance threshold and you will coming plans before deciding and that method helps to make the very sense for you. However, if you’re in the marketplace getting property, this will be an enjoyable experience to understand more about the options.

Angelica Einfach try senior editor having Controlling Your bank account, in which she writes and you can edits stuff to the a variety of private money topics. Angelica prior to now held modifying positions on Simple Buck, Focus, HousingWire or other financial e-books.

No Response to "Ways to get a beneficial 6% (otherwise down) home loan rate nowadays"